Bring Excellency With Our Expertise

Our dynamic and energetic team always strives to work to bring the best possible for your team. From the scratch we plan, organize, and create seamless human resource solutions for you.

Our dynamic and energetic team always strives to work to bring the best possible for your team. From the scratch we plan, organize, and create seamless human resource solutions for you.

Enquiry@hrhelp.in

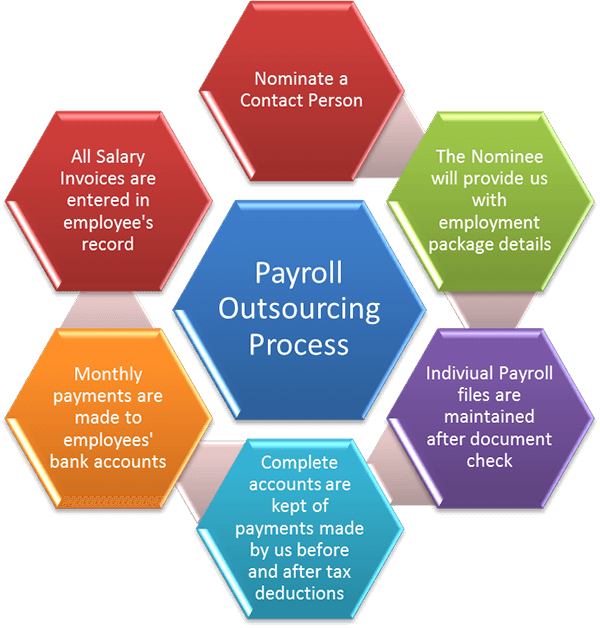

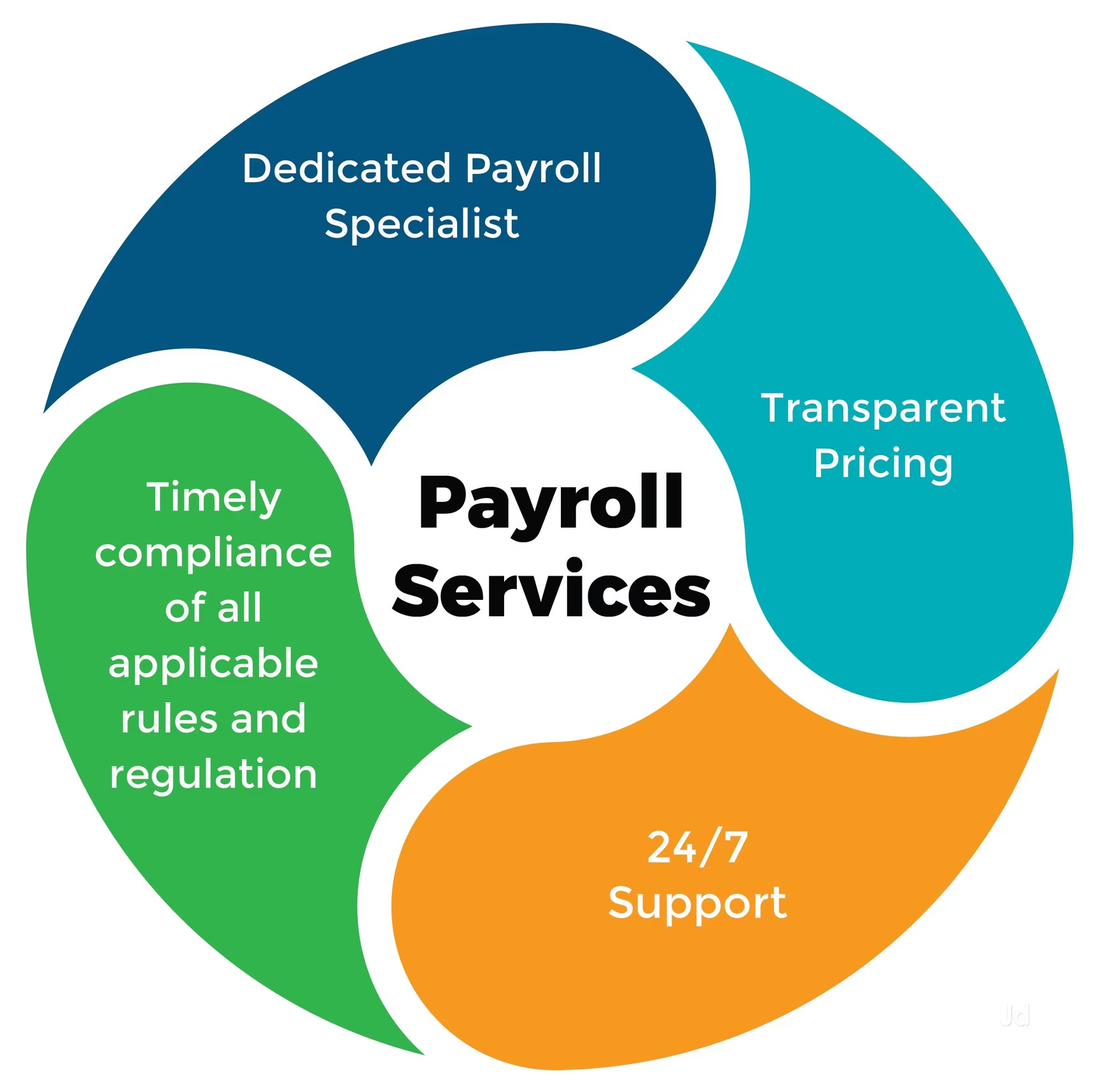

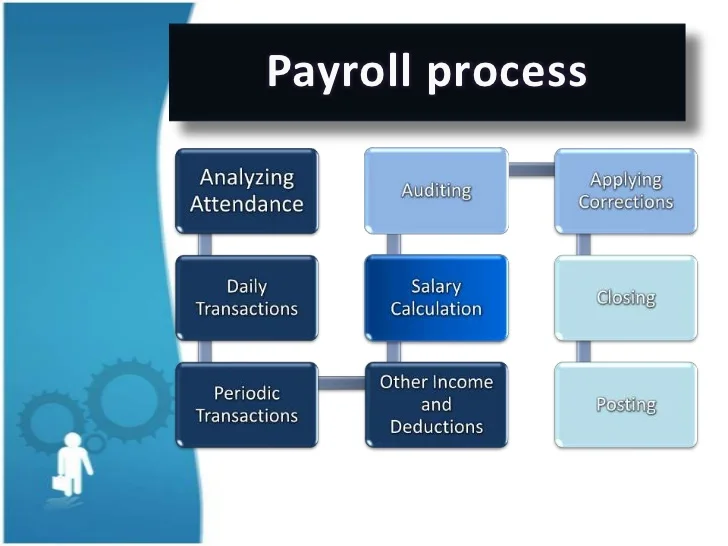

Our end-to-end payroll solutions are meticulously designed to ensure seamless Payroll processing while rigorously adhering to the Contract Labour (Regulation and Abolition) Act (CLRA) and other labor statutes. We specialize in managing payroll for businesses employing contract labor, ensuring compliance with wage regulations, statutory benefits, and working conditions mandated under CLRA. From accurate wage calculations to timely disbursements and mandatory documentation, we eliminate compliance risks, fostering trust and legal conformity.

CLRA Compliance Expertise

Navigating the complexities of contract labor regulations is simplified with our deep expertise. We ensure proper classification of workers, adherence to minimum wage standards, overtime calculations, and statutory deductions (PF, ESI, bonuses), while maintaining meticulous records for inspections or disputes.

Real-Time Online Auditing

Our digital auditing platform provides continuous, transparent monitoring of payroll processes. Automated checks flag discrepancies instantly, generating audit-ready reports and maintaining an immutable record of transactions. Businesses gain 24/7 access to dashboards for real-time compliance tracking, ensuring transparency and proactive risk management.

Offline Auditing by Labour Auditors

Complementing our technology, our certified labour auditors conduct thorough on-site inspections. They verify physical records, interview staff, inspect workplace conditions, and validate compliance with CLRA and other labor laws. This dual-layer approach—combining digital precision with human expertise—ensures holistic adherence and prepares businesses for regulatory inspections.

Data Security & Risk Mitigation

Secure Infrastructure: We deploy advanced encryption methods and secure storage protocols to protect sensitive payroll data.

Error Reduction & Fraud Prevention: Automated validations and systematic checks reduce the risk of errors and potential fraud, ensuring that every transaction is recorded accurately.

Legal Risk Management: Regular internal audits and expert reviews help mitigate exposure to non-compliance penalties and labor disputes.

Scalable & Tailored Solutions

Multi-State & Multi-Entity Readiness: Our services accommodate businesses operating across various regions and jurisdictions, adapting dynamically to local wage laws and tax implications.

Custom Workflow Integration: We work closely with your HR and finance teams to integrate our payroll system with your existing ERP or HRMS solutions, creating a seamless operational environment.

Vendor Integration: Whether you use industry-specific tools or ERP systems like Simpliance or Aprajitha, we ensure our solution interoperates smoothly with third-party compliance and auditing platforms.

Key Features.

Accurate Salary Computation & Processing

Automated Calculations: Our system uses pre-validated formulas to compute gross salaries, multiple layers of deductions (PF, ESI, TDS, Professional Tax, etc.), and net pay.

Attendance & Leave Integration: Real-time synchronization with attendance data ensures adjustments for overtime, absences, leaves, and other variable factors.

Robust Compliance Assurance

Legislative Adherence: We keep your payroll aligned with the latest updates to labor laws such as the Minimum Wages Act, Payment of Bonus Act, Gratuity Act, and more.

Dynamic Updates: Our compliance module is designed to automatically update in line with any changes in government mandates, ensuring that your payroll processes are always current.

Audit-Ready Processes: We generate detailed audit trails and reports that facilitate both internal and external compliance checks.

Integrated Auditing & Reporting Tools

Comprehensive Reports: From detailed payslips to statutory payroll registers, our solution produces all necessary documents required for regulatory filings.

Real-Time Monitoring: Interactive dashboards and periodic compliance reports provide stakeholders with real-time insights into payroll metrics and adherence, ensuring complete transparency.

Customizable Audit Workflows: Easily configure audit checkpoints and compliance reviews tailored to the specific regulatory framework applicable to your business.

Methodologies & Technologies

Automation & Software Integration:

Utilizing a blend of custom-developed macros, cloud-based payroll solutions, and industry-leading software integration, our system automates the majority of payroll tasks, reducing manual intervention and streamlining workflows.

Continuous Compliance Monitoring:

Our platform employs continuous monitoring tools that perform real-time checks and flag discrepancies instantly, allowing proactive adjustments before any regulatory deadlines are missed.

Transparent Reporting & Support:

We provide exhaustive documentation and customizable dashboards that simplify the monitoring of payroll metrics, with ongoing support from our dedicated compliance team.

Scalable Growth:

Our solution grows with your business, handling increasing workforce complexities, multi-state operations, and evolving compliance requirements effortlessly.

Benefits to Organizations

Enhanced Operational Efficiency:

Automation and integration reduce manual entries and administrative overhead, freeing up resources for more strategic tasks.

Reduction of Legal and Financial Risks:

With built-in compliance checks and error detection, your risk of incurring penalties or facing legal disputes diminishes significantly.

Improved Employee Trust and Satisfaction:

Transparent, error-free payroll processing ensures that employees receive accurate payments and clear breakdowns of deductions, fostering a sense of trust and reliability.

As a trusted service provider, we deliver a deeply integrated payroll processing solution that satisfies rigid compliance mandates while optimizing operational efficiency. Our approach is holistic—combining advanced technology, expert knowledge, and proactive auditing to ensure every component of your payroll not only meets but exceeds regulatory standards. With our service, you can be confident that your payroll processes are secure, compliant, and aligned with the strategic needs of your business.

If you’re interested in learning more about how our service can be tailored to your specific organizational requirements, or if you’d like to see case studies detailing our compliance successes, let’s discuss further. There are also additional areas, such as advanced analytics for payroll trends or integration with HR benefits management, that we can explore to add even more value to your operations.

We treat our customers as our partners. That helps them explain their ideas fluently and grow their organization to the fullest with the best support.

Hear What Our Clients Are Saying About Working With Our Team.

“I came up with the idea to develop a useful app that will bring smiles to millions of minds. The team of HR Help Team has heard my side of the story and turned that into an interactive application. I will suggest this company as well.”

Mario Speedwogan

May 21, 2020